The Finances on Wednesday will reveal how a lot tax every of us can pay and the way a lot the federal government will select to spend on providers just like the NHS, faculties and transport.

BBC Information has been talking to folks with a spread of incomes about what they need from the Finances and, in some circumstances, how they worry they may very well be impacted.

If there are points you want to see coated, you will get in contact through Your Voice, Your BBC Information.

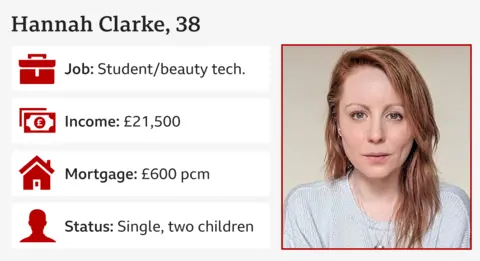

Mum-of-two Hannah Clarke from Rutland within the East Midlands was juggling two part-time jobs however not too long ago began learning full-time for a midwifery diploma. She additionally works six to eight hours every week as a magnificence technician.

She takes house about £1,800 a month, largely through a pupil mortgage which she does not pay tax on. She says this nearly covers her mortgage funds – which went up by a 3rd earlier this yr – payments and gas.

“I nearly make ends meet, but it surely is not simple and I do typically need to ask for assist,” she says.

She would really like free faculty meals to not be means examined however failing that, says the eligibility threshold must be lowered. She additionally says if gas responsibility goes up then the additional price per litre of petrol or diesel “ought to completely not be handed on to drivers”.

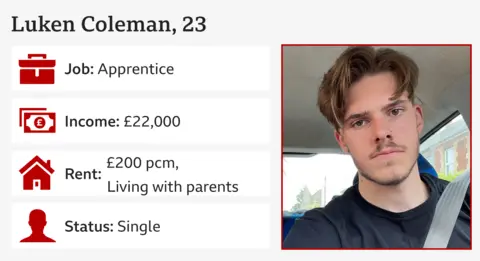

‘I can not transfer out on £1,500 a month’

Luken Coleman works as a Stage 3 enterprise administration apprentice for a recruitment company, incomes about £1,500 a month. Beforehand he labored in retailers and in handbook labour jobs.

He works full-time Monday to Friday and goes to varsity in the future a month.

Luken lives in Newbury together with his dad and mom and pays them £200 a month hire. Whereas he pays all his personal payments, he can not afford to maneuver out and says he want to see apprentices receives a commission extra.

“The common hire the place I stay is between £700 to £900 per 30 days. If I did transfer out, I would have to maneuver additional away, so I would want a automobile.”

As somebody nearing his mid-20s, he says it might probably really feel such as you’re not attaining a lot when you’re nonetheless residing at house.

“It is a psychological well being factor. Cash-wise, apprentices are paid much less since you are studying on the job, however it might probably make you are feeling much less about your self when you’re not totally unbiased.”

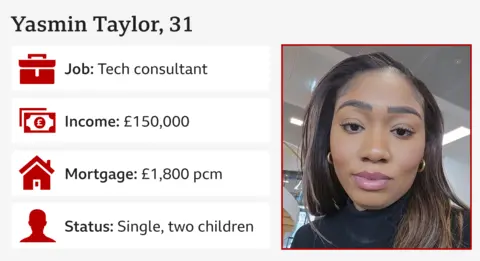

‘I make £7,600 a month however £2,600 goes on childcare’

Yasmin Taylor from Kent is a tech marketing consultant and single mom of two younger youngsters.

Her largest outgoing is £2,600 per 30 days on childcare. The youngsters’s father additionally helps with prices.

“I studied and labored laborious to get a job that pays an important wage, however I really feel like I’m being punished for having youngsters,” she says.

Due to her £150,000 wage, Yasmin doesn’t qualify for Youngster Profit funds, or assist through tax-free childcare or 30 hours free childcare.

She acknowledges that her earnings classifies her as a excessive earner, however says: “You continue to need to pay the gasoline and the electrical and that is gone up quite a bit.”

One in all her foremost considerations is round power payments this winter.

She can also be desirous about what the chancellor could do on capital good points tax (CGT). Though she just isn’t topic to CGT now, the subsequent step in her profession can be to change into a associate at her agency, which might contain her shopping for shares within the firm – which can later be topic to CGT if she have been to promote them.

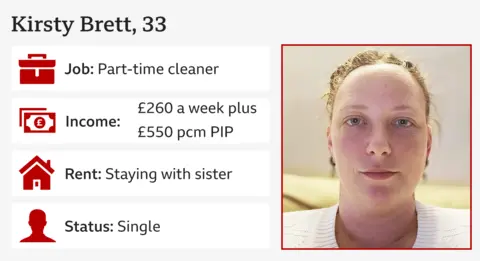

‘I can solely afford a caravan on £1,590 a month’

Kirsty Brett works part-time as a cleaner in a care house, incomes the minimal wage of £11.44 an hour.

She not too long ago moved in along with her sister in Bury St Edmunds in Suffolk whereas she seems for brand new lodging, after leaving her outdated job as a carer in Essex.

Kirsty has osteoporosis, which made her work tough, and likewise discovered it too costly residing in Essex. She receives £550 a month in Private Impartial Funds.

She want to see an increase within the Nationwide Dwelling Wage.

“Individuals must be paid at the very least £15 an hour. As a result of the price of residing has gone up. That may assist lots of people.

“The wage they class as minimal wage – I don’t see the way it sustains somebody.”

She is now taking a look at “the most cost effective choices” for someplace to stay. She says she’s discovered renting a one-bedroom flat prices about £1,300 a month, so Kirsty is as an alternative taking a look at renting a caravan for round £800 a month.

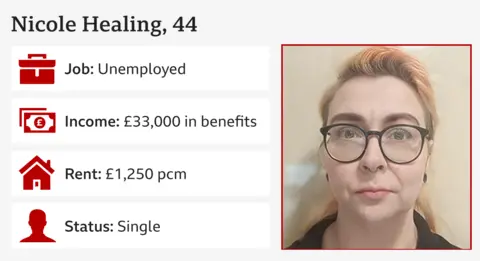

‘I get £2,750 in advantages and I am freaking out over cuts’

Nicole Therapeutic rents a one-bed flat in Brighton for £1,250 a month.

Nicole beforehand labored as a civil servant and in digital advertising, however hasn’t been capable of work for the previous few years as a result of a number of disabilities, together with a connective tissue dysfunction that causes their joints to dislocate.

Nicole receives Employment and Assist Allowance of £1,042, Private Impartial Funds of £798, and Housing Good thing about £917 per 30 days.

Although they really feel in a “lucky place” at present, Nicole says: “I really feel I’m on the mercy of the DWP.”

Nicole is “utterly freaking out” about attainable cuts to advantages within the Finances and what that would imply for them.

“I’m fearful in regards to the adverse rhetoric within the media about disabled folks in receipt of advantages.”

They are saying their power invoice has gone up considerably in the previous few years and they’re frightened their hire will even improve.

“I’m not ready to make use of my PIP for what it’s meant for use for. Half of the fee goes in direction of my hire.”

Nicole needs the Finances to make clear what assist is deliberate for disabled folks, and is hoping for a cap on power payments this winter.

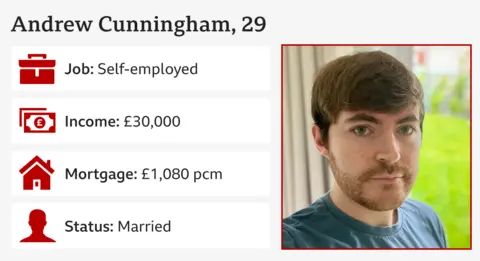

‘I attempt to save as a lot of my £1,920 a month as I can’

Blogger and net developer Andrew Cunningham lives together with his husband in Glasgow. He describes themselves as “center earners however diligent savers” who’ve been investing of their particular person financial savings accounts (ISAs) and their pensions to fund their retirement.

He’s involved about rumours that there may be a cap on the amount of cash you possibly can maintain tax-free in an ISA within the Finances. “That may hit us and can be an enormous disincentive to save lots of.”

He’s additionally frightened that any flat fee launched on pension tax aid would hit center earners.

As he’s self-employed, Andrew has arrange a self-invested private pension. A single fee tax aid would imply much less cash going into his pension.

“We live our lives assuming we gained’t get a state pension once we get to pension age, at the very least not within the type it’s now,” he says, mentioning that spending on the state pension has grown over time as a proportion of the federal government’s finances.

He thinks in years to return, the federal government may need to boost the state pension age once more, or reduce the quantity of profit you get.

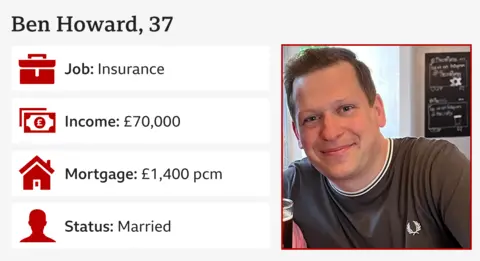

‘We earn £100,000 and count on to be worse off’

Ben Howard and his spouse Sarah from Bristol expect their first youngster in February. They’ve a joint earnings of £100,000. In September, their mortgage repayments went up by 60% to £1,400.

Ben says they’re “snug”, however thinks the federal government ought to do extra round the price of childcare, as a result of in some circumstances, “it is extra environment friendly for [parents] to not work”.

“However that places us again when it comes to what our profession aspirations are.”

Ben just isn’t totally satisfied that Labour will hold its promise of not elevating taxes on “working folks”.

“Am I going to see tax on my pension contributions, any type of stealth tax?”

He expects to be worse off after Finances day. “They are going very massive on enterprise and rising the economic system, and I get that, however nothing’s resonating with me and my pay packet.”

‘My pension of £1,200 a month does not cowl my outgoings’

Allana Lamb is a military and navy veteran and a retired social employee. She is a few kilos over the brink for pension credit score so she is not going to get the winter gas fee this yr.

“I’m very involved in regards to the authorities stopping it,” she says. “Sure, [the state pension] is triple locked but it surely does not cowl the price of residing.”

She feels “the wealthy are going to get richer” from this Finances and that “these on the backside of the pile or on the cusp of the underside” will probably be hit with extra taxes.

Allana will get each the complete state pension and a small military pension, totalling £1,200 a month. She says her earnings is not sufficient for all of her outgoings, and expects her mortgage to “nearly double” within the subsequent few years. “That’ll put me in adverse month-to-month outgoings.”

Allana additionally thinks the brink for getting some council assist to pay for social care prices must be raised. Presently folks with property as much as £23,250 qualify. Labour has already scrapped plans to extend this.